Five 5 Alternative Loan Apps Like Earnin Review

Over half of all working Americans, including those who make betwixt $fifty,000 and $100,000 a year, alive paycheck to paycheck.

If you need a couple of extra hundred dollars before you become paid and are thinking about taking out a cash accelerate, hither are 10 of the best apps right now.

Best cash advance apps

With millions of people struggling to go along up with their bills, going into debt isn't exactly uncommon. That'due south why many people consider short-term options like installment or payday loans to go along adrift financially.

But as engineering science continues to evolve and many financial services become digital, these high-involvement, short-term loans aren't the only solution to fiscal hardship. Instead, cash advance apps serve as a temporary, immediate financial solution for those who need a little actress aid keeping up with the bills.

If you've constitute yourself in a tight spot financially, here are some of your best options right at present.

Best for taking out a big greenbacks advance: Possible

Possible is a cash advance app that besides offers short-term installment loans to consumers. It is BBB-accredited with an A- rating and 4.53/5 stars. Check out the reviews here.

Pros:

- Loan amounts are larger than boilerplate: They'll advance upward to $500 inside minutes (minimum $50)

- No credit score required

- It may exist used to rebuild credit

- Avert overdraft fees

- Flexible repayment terms with optional delayed payment

Cons:

- Only available in 15 states

- App links to a checking account

- Loan terms vary based on state

- Installment loan with higher interest rates (up to 257.00% April)

- Cash advance amount varies by state and may be smaller depending on where yous live

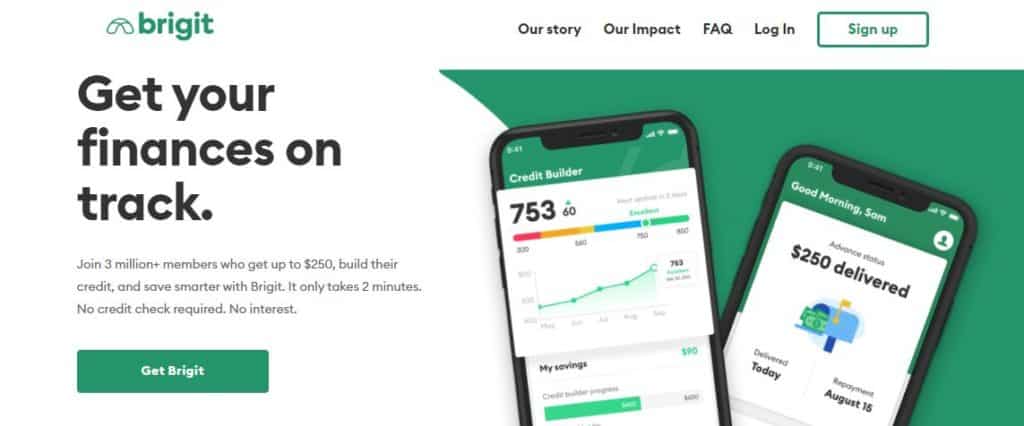

Best for help with budgeting: Brigit

Established in 2019, Brigit is a fast-growing company that offers cash advances to eligible individuals. On Brigit'south BBB folio (here), information technology has a B rating with 1.57/v stars and 8 customer reviews. Still, the app has iv.5/five on Google Play with 52,000+ reviews. It also has 4.viii/5 on the Apple App Store with 140,000+ reviews.

Pros:

- Upward to $250 in cash advance (funds available within 1 business day)

- No credit check or involvement

- Option to extend the due appointment on the first loan once without penalisation (with up to iii delayed payments with proficient borrowing history)

- Optional automated advances as function of the Brigit Plus programme ($10 monthly fee)

- Flexible repayment, instant deposit, credit monitoring and identity theft insurance through the Brigit Plus plan

- Free financial resources (ex. tips and ways to earn more cash)

Cons:

- App automatically withdraws the money owed from the adjacent paycheck

- Must testify proof of income with 3+ direct deposits in a row from an employer

- Active checking account required with a positive balance

- Must achieve 70/100 on Brigit'south unique scoring organisation to qualify for cash advance

- May be difficult to deactivate or shut the account

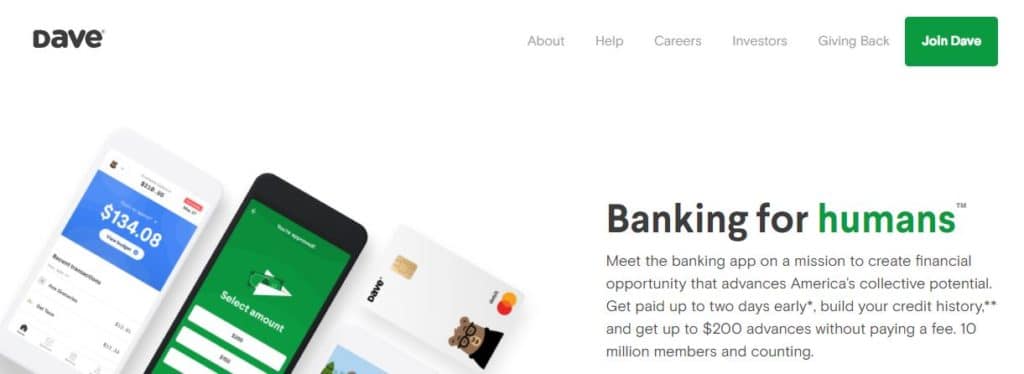

Best for improving your fiscal weak spots: Dave

With over a million active members, the Dave app offers a highly reputable online checking business relationship that likewise offers cash advances. Information technology is BBB-accredited (cheque it out here) with a B rating. It only has i.27/five stars out of 218 customer reviews on BBB. However, information technology has four.8/5 on the Apple tree App Store with 490,000+ reviews and a like score on Google Play.

Pros:

- Up to $200 cash accelerate to avoid account overdraft

- No credit check

- No interest

- Automated budgeting based on boilerplate expenses

- Free (optional) subscription to LevelCredit, which reports payments and financial action to the credit bureaus to help build credit

- No minimum account residue required

- Charity-focused company that makes monthly donations

- Average users relieve around $500 in yearly fees

- Free budgeting tools and other resources

Cons:

- $ane monthly membership fee (plus optional tips)

- Automatic withdrawal to repay the greenbacks advance

- Credit-building option simply available to those with direct deposits and a Dave Spending Account

- Some concerns related to billing and product issues, though this is common among all cash advance apps

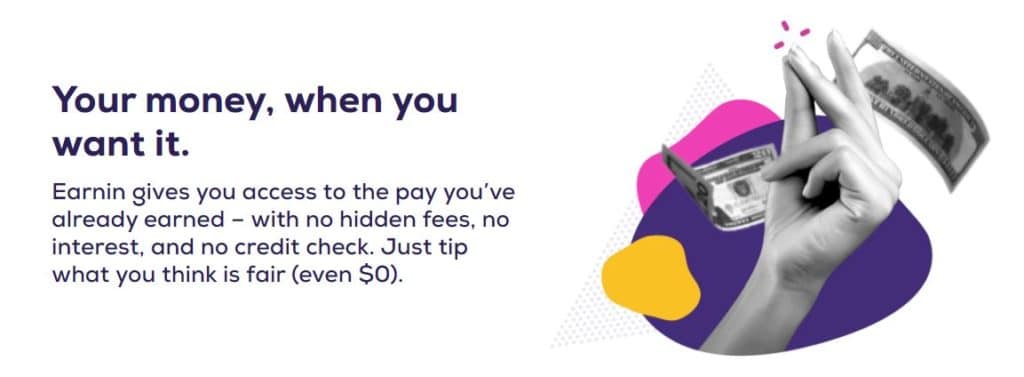

Best for paying equally little as possible to infringe: Earnin

A highly reputable lender with largely positive reviews, Earnin has been in concern for the past seven years. It has around i.3 1000000 active users. On BBB (page found here), Earnin is accredited with an A rating and 4.06/five stars.

Pros:

- Maximum $100 a solar day or $500 per pay menstruation cash advance

- No credit score required

- Involvement-free cash advance

- No hidden fees

- Client-commencement approach

- Tin can get up to 10% cashback by linking a valid credit menu (at participating locations)

- Operated through FDIC-insured institution

- Alerts for low account balance with the selection for automatic $100 greenbacks accelerate to avert overdraft fees

Cons:

- Must get paid regularly (monthly or biweekly)

- Despite high ratings, some customers experience bug with the app and billing

- Automatically withdraws the residue owed (plus optional tips) from the adjacent paycheck

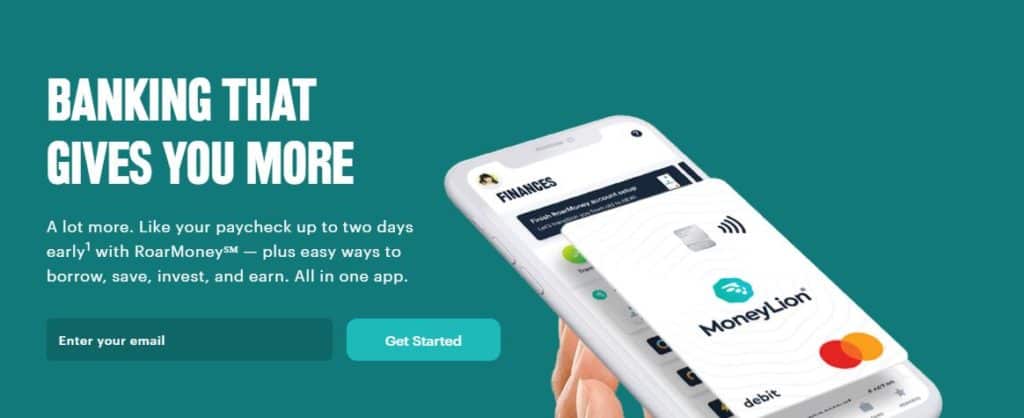

Best for multiple financial products: MoneyLion

MoneyLion is an online banking service that offers savings accounts, investment accounts and cash advances. It has a B- rating on its BBB page (institute hither) and is not accredited. On BBB, information technology has 4.69/5 stars with over 2,400 client reviews.

Pros:

- More than a cash advance app with the RoarMoney business relationship, a savings account and an ETF (exchange-traded funds) investment business relationship

- $250 borrowing limit with instant admission to funds through its Instacash feature

- No credit bank check

- No involvement

- 24/7 Instacash feature for cash advances

- Access to paycheck upwardly to 24 hours early via RoarMoney account

- No business relationship minimum residue

- Choice to build investment portfolio based on individual risk tolerance

- Cashback rewards through RoarMoney account

- Optional Credit Architect Plus account for those who need a loan upward to $i,000 and desire to build credit

Cons:

- $1 monthly administrative fee for the RoarMoney business relationship

- $1 monthly fee for the ETF account

- 5.99% to 29.99% APR on Credit Builder Plus account

- Credit Build Plus business relationship costs $19.99 a month

- Some recent complaints involving payment issues and poor customer service

All-time if yous also need extra money direction help: Empower

Empower is more a greenbacks advance app. It is a growing fintech company that offers automatic savings and budgeting tools, as well as access to a big network of ATMs. Its website promises that "The Empower Card is the only carte du jour you'll ever need."

Pros:

- Cash advances of up to $250 with no involvement

- Collect your wages up to two days faster (this is carve up from the cash advance feature)

- Empower Perks allow you earn up to x% greenbacks back on places where you already spend money and items you already buy

- Go unlimited access to more than than 37,000 MoneyPass ATMs across the U.s.

- You'll pay no overdraft fees or bereft funds fees, and there are no account minimums

- Automatic Savings characteristic keeps track of your income and expenses, so — using that information — will transfer money into your AutoSave account.

Cons:

- The monthly fee of $8 is more expensive than some of the other options

- There's no way to deposit greenbacks or checks into your Empower account

- Information technology'south a mobile app merely; there is no desktop version

Best for fast access to your paycheck: Varo

Varo is a full-service online bank known for granting users early access to their paycheck. It likewise offers cash advances. Information technology is BBB-accredited with an A+ rating and iii.92/5 stars out of 377 client reviews. Bank check out Varo'southward official BBB page here.

Pros:

- Up to $100 in cash accelerate (minimum $20)

- Complete online banking service

- With direct deposit, you can access your paycheck as shortly as your employer transfers the money over (up to 2 days earlier than anyone else)

- No involvement or hidden fees

- No credit check required

- No minimum Varo bank account residue

- Early on access to tax refund through direct deposit

Cons:

- Small cash advance limit

- Some complaints with using the service

- Must accept an agile bank account at least ane month quondam with at to the lowest degree $one,000 in monthly straight deposits

Best for flexibility: Chinkle

Chime is a fast-growing fintech visitor with overwhelmingly positive reviews on Google Play or Apple's App Stores. On BBB, it has a B rating and is not accredited. Check out Chime's full BBB page here.

Pros:

- Up to $200 cash advance (involvement-gratis)

- Aforementioned-24-hour interval access to funds via direct eolith

- No credit or bad credit is OK

- Full-service bank account for things like greenbacks advance and online beak pay

- No overdraft, monthly or other subconscious fees

- Provides banking alerts to let you know when y'all get paid

- Optional to set up automatic savings for a portion of each paycheck

- Works in conjunction with other apps while y'all build financial/credit history

- 24/seven client back up

Cons:

- Low initial cash advance of $20 (increases over time with good money habits)

- Many recent complaints from customers not receiving funds or accounts being airtight without a clear reason

Best loan app that requires your employer to sign up: Even Instapay

Created by Walmart in response to the COVID-19 pandemic, Fifty-fifty is more than merely a cash accelerate app. It's besides a fiscal planning tool designed to assistance users budget and salvage coin. The app works past getting payroll data from a qualifying employer to then provide a small greenbacks advance.

Even is BBB-accredited (cheque out the BBB page here) with an A+ rating. However, at that place are no customer reviews on the site. On the Apple App Store, Fifty-fifty has 4.9/5 stars. It has 4.8/5 stars on Google Play.

Pros:

- Instapay, a feature of the Fifty-fifty app, gives immediate admission to money that's been earned simply not yet paid

- Maximum 50% of earned wages available

- No interest on cash advance

- Funds are available for option up at any US Walmart or via directly deposit within 1 business day

- May get an advance with a joint bank account

- Easy online application

- Free online fiscal tools to help track money, spending habits and gear up a upkeep

- Option to automatically set aside money for savings

Cons:

- $8 a month Fifty-fifty Plus membership fee to qualify for an Instapay cash advance

- Instapay only offered through an eligible employer

- Agile banking concern account and debit card access required

- Must accept a regular source of income with direct eolith

- Variable loan terms

- Vague on which employers are eligible

Runner up: DailyPay

With DailyPay, employees build a residuum with each 60 minutes of work they complete. They can and so dip into that balance before payday.

Pros:

- You tin access your pay from Day one, and have information technology sent to whatever account instantly or on the next business organization solar day.

- No late fees, overdraft fees or payday loan interest and fees.

- You can transfer coin at any time

- Other financial tools and services are available

Cons:

- If your employer doesn't participate, you tin can't use the service

- It's costless to sign up, merely you pay $1.25 every fourth dimension you transfer money

What is a cash advance app?

Due to the appearance of fintech (financial technology), people no longer have to rely solely on a trip to the bank branch or storefront lender for a loan. Now, mobile banking allows many companies to offer financial services and products online.

Cash accelerate apps, also sometimes known every bit payday advance apps, are one of the most pop digital financial services out there. These apps provide well-nigh instant cash, giving the user access to money they've already earned but oasis't however received from their upcoming paycheck. For people who need to pay a neb before payday or have a financial emergency, a cash advance app could be a good option.

Most cash advance apps are free to use, though some accuse a minor membership or monthly fee. Unlike many lenders, very few cash advance apps charge interest or loan origination fees. Even those apps that do charge a small fee are unremarkably much more affordable than other short-term loan options.

That doesn't hateful they're a long-term solution, however. Fifty-fifty a hundred dollars can add upwards over time, especially if yous regularly accept out an advance from your paycheck and don't take a good way to pay information technology dorsum.

Also, keep in mind that some companies merits to offering cash advances, but they operate more like payday lenders with sky-loftier fees and unreasonable loan terms.

Unlike many other short-term lenders, the cash advance apps we're recommending are highly reputable and legitimate.

How do greenbacks advance apps piece of work?

Cash advance apps requite borrowers paycheck advances, or early access to coin they've earned but haven't received yet. They are particularly useful for those who may otherwise miss a payment on a bill or end upward with a late fee or overdraft fee.

Most greenbacks advance apps have a borrowing limit that falls somewhere betwixt $100 and $500. People who demand extra cash early on can request an accelerate on their paycheck (usually involvement-costless), but they must pay it dorsum on their adjacent payday. Some apps will automatically withdraw the funds from the borrower's business relationship when the fourth dimension comes.

Since greenbacks advance apps rarely charge interest or come with other fees, many people consider them a meliorate alternative to other short-term funding options like payday loans.

How quickly can I become my cash advance?

Afterward you find a cash advance app you like, the get-go matter you need to do is set up an business relationship. This usually involves a simple online application that requires bones information such as:

- Identification (name, SSN, date of birth, etc.)

- Contact information (address, phone, email)

- place of employment and/or employer

- Banking data

Most issuers' applications but take a few minutes to complete and an additional ane or 2 business organisation days to corroborate. In one case approved, you can request a greenbacks accelerate. Since these apps are designed with speed in mind, it tin take anywhere from a few minutes to a couple of business organisation days to receive the funds. Some apps charge a pocket-sized fee for instant access.

What to look for in a cash advance app

Although most cash advance apps operate nether the same kind of thought, not all are created equal. Here's what to look for when deciding on which cash accelerate app to use:

- Borrowing limits: Most apps have a borrowing limit betwixt $100 and $500. Some apps accept a lower starting limit that tin increase with time and employ. Check the requirements to see how much you can borrow.

- Turnaround time: Depending on the app, you could receive the greenbacks accelerate within minutes of requesting it. Or information technology could take a couple of business days to come through. Some apps accept a premium pick for instant funding, but this usually includes a pocket-size fee.

- Fees: For the most function, cash advance apps are complimentary to use. They also don't usually charge involvement since they aren't a real loan. Some apps do take a feature for an optional tip (commonly a few dollars) to aid keep them running. Other apps, and those with premium features, may charge anywhere from $one to $10 a month.

- Requirements: Most apps have minimal eligibility requirements. Common requirements include a minimum credit score, direct deposit from a regular employer and an active banking concern account. Most apps require users to exist 16+ years former and a Usa citizen.

- Other features: Many apps offer online fiscal resources and tools to assistance users with budgeting, saving and spending. Some apps operate more similar a traditional banking company with a checking and savings account. A few apps offering an investment business relationship and means to build a diverse portfolio.

- Reviews: If a cash advance app sounds besides good to exist true, chances are it is. Cheque out online reviews at sites similar BBB.org, Google Play Shop and the Apple App Store to see what users are saying.

Should you lot apply a cash accelerate app?

If you occasionally observe yourself strapped for cash at the stop of the month, a cash advance app could aid you become through until your next paycheck. After all, cash advances are primarily meant for paying modest bills that are due before yous become paid.

Just if you lot regularly struggle to go on up with payments, a cash advance app is not a viable solution. These apps are designed to provide immediate relief to a small-scale, brusk-term financial problem. They are not meant for ongoing utilise.

Instead of relying on greenbacks advances, try to get a handle on your upkeep and spending habits. If y'all're often short on coin just before your next paycheck, you may demand to adjust your upkeep or consult a financial advisor to aid turn things around.

There are likewise other options out there. Wait into starting a side hustle or inquire friends or family for a loan if you need to.

Greenbacks advance apps vs. payday loans

Payday loans and greenbacks advance apps are similar in a couple of big means.

- Both are short-term options designed to help you cover modest bills or an emergency expense apace.

- Both have minor borrowing limits, though payday loans sometimes have a higher limit at $one,000.

- Payday loans and cash advances must be repaid in a lump sum with the next paycheck.

Different greenbacks advances, payday loans come with high involvement rates that are often in the triple digits. They also commonly have lender fees, late payment fees and other subconscious costs. For many people, a $300 payday loan tin hands get a couple of thousand dollars by the cease. Since most people tin can't afford to pay dorsum the loan as scheduled, they end upward in a debt trap. In fact, more than 90% of borrowers regret taking out their payday loan.

It is still possible to finish up in a cruel wheel of debt with a cash advance, or with any other curt-term financial option. Notwithstanding, greenbacks accelerate apps are usually more customer-friendly and do not accept the same predatory lending practices as payday loans.

Still, it's important to know what y'all're getting to earlier y'all take out a cash accelerate or loan. The more prepared y'all are, the less likely yous are to fall into a debt trap.

For more information on some other payday loan alternatives, sentry this video:

Long-term risks of cash advance apps

Cash advance apps accept minimal risks in the short-term or with sometime or occasional apply. Withal, relying on these apps over and over again comes with some serious fiscal risks.

For 1 thing, fifty-fifty the small-scale fees that come with some greenbacks advance apps can add upward. A dollar or two may not seem like much at commencement, merely if you're already struggling to keep up with your monthly bills, every little bit counts. The more you spend on things like instant funds, administrative fees or fifty-fifty tips, the less you have for your adjacent paycheck.

For example, say y'all infringe $150 from your paycheck to help cover the following month'due south electricity bill. When y'all go paid once more, the app deducts that $150 (plus any tips) from your paycheck. This deduction could make it difficult for you lot to pay for upcoming bills or groceries.

More borrowing options

Payday alternative loans

Payday Alternative Loans (PALs) are given out through federal credit unions instead of predatory payday lenders, making them much more affordable. Their purpose serves the same need: to loan small amounts of coin to borrowers who demand cash between paychecks. Unlike payday loans that must be paid in full by your next payday, PALs are installment loans where yous'll take a payment plan, and interest rates are capped at 28%.

Peer-to-peer loans

Peer-to-peer lending is some other form of personal loan, but in this instance, individuals are loaning money to borrowers directly rather than through a depository financial institution or credit union. Borrowers become to the lending website, fill out an application, and are assigned a take chances category dependent on their financial profile. Investors offering loan terms and interest rates that the borrower can have or refuse. If the offer is accepted, the money is transferred through the website.

Personal loans

Personal loans are flexible unsecured (no collateral) loans that tin be relatively affordable when you need cash for full general expenses. While it can be difficult to qualify for one with a depression credit score, it'due south still possible.

Personal loans are usually issued for amounts between $500 and $100,000, with interest from 3% to 36% APR. The repayment periods are roughly two to five years.

The bottom line

Ultimately, if y'all observe yourself relying heavily on short-term personal finance options like cash advances, you may need to step back and wait at the bigger pic. If you only need them every now and and then, a cash accelerate shouldn't come up with major risks.

FAQs

What happens if you don't repay a greenbacks advance app?

Failure to pay back a cash advance app may become you banned from using the service. Yet, though the app doesn't accuse fees, it volition continue trying to withdraw money from your bank account, which could rack up overdraft fees.

Volition a cash advance app look at my credit score?

Many greenbacks advance apps don't bank check your credit or FICO score to evaluate creditworthiness.

Instead, the app links to your bank account, where it tin track your financial history. Information technology will examine your direct deposit payments, monthly expenses and spending habits to determine eligibility.

What if a payday advance app doesn't lend me enough?

Unfortunately, the loan amounts offered by cash advance apps are very modest. If yous need to borrow more than the maximum corporeality, you'll need to utilize for personal loans or endeavor a credit menu greenbacks advance.

What'due south the departure between a cash advance app and a payday loan?

A cash advance is a curt-term cash loan you accept out through your credit card. A payday loan is a short-term loan that typically comes with just a few application requirements and a quick turnaround time.

What if a payday advance app won't lend me enough?

Unfortunately, these cash advance apps only offer small-dollar loans. If you need more than than the maximum amount offered, you'll need to utilize for personal loans or try a credit carte cash advance.

Will using a greenbacks advance app help or hurt my credit score?

Similar any apply of your credit cards, a greenbacks advance can affect your credit score, especially if you lot aren't careful about how much money you obtain and when you pay information technology back.

What is Instacash?

Instacash is a brusque-term cash float from MoneyLion. You can get upwards to $250 instantly to cover an unexpected expense or to use for a fun opportunity at 0% interest. Traditional payday accelerate loans often charge ludicrously loftier involvement rates that can go as high as 790% per year in some states.

Source: https://debthammer.org/best-cash-advance-apps/

0 Response to "Five 5 Alternative Loan Apps Like Earnin Review"

Post a Comment